In the New Energy Era, Does the ICE Vehicle Parts Market Still Have a Future?

As the wave of new energy vehicles sweeps across the globe, discussions about the future of internal combustion engine (ICE) vehicles have never been more intense. Recently, in conversations with numerous domestic and international distributors, we have repeatedly heard several similar concerns:

As new energy vehicles continue to sell better and better, will the ICE aftermarket enter a downturn earlier than expected?

How much longer can the business of ICE vehicle parts continue?

Such anxieties are understandable. With the continuous growth of NEV sales and the accelerating transformation of the industry, market sentiments are constantly being amplified.

However, before drawing any conclusions, we need to clarify a logical point that is often confused and most easily misunderstood: Strong NEV sales ≠ No business for ICE vehicle parts

The rising sales of NEVs change the structure of the new car market, whereas the auto parts aftermarket serves the existing vehicle fleet already on the road. What truly determines the scale of the aftermarket has never been new vehicle sales, but rather the total vehicle population (parc) and the average vehicle age, which drive actual maintenance and repair demands.

Global Vehicle Parc: ICE Vehicles Remain the Dominant Majority

For the automotive aftermarket, the existing stock is the core determinant of business scale.Although new energy vehicles have developed rapidly in recent years, ICE vehicles still define today' s stock market in terms of vehicle ownership.

According to forecasts by the International Energy Agency (IEA),the global NEV parc is expected toreach approximately 85 million vehicles in 2025, accounting for only around 5-6% of total global vehicle ownership. Meanwhile,Gartner predicts that the global stock of battery electric vehicles (BEVs)will reach nearly 59.48 million units in 2025, representing only about 4% of the global vehicle parc.

Even in China, the market with the highest NEV penetration, NEV ownership reached 43.97 million vehicles by the end of 2025, accounting for 12.01% of the country' s total vehicle parc.Among them, battery electric vehicles (BEVs)will account for 30.22 million units,representing 68.74% of all NEVs and approximately 8.26% of the total vehicle parc. This also means that internal combustion engine (ICE)vehicles will still dominate the aftermarket with an overwhelming share of 87.99%. (Source: Traffic Management Bureau of China's Ministry of Public Security)

Even if the world aims to achieve parity between NEV and ICE vehicle ownership, long-term forecasts from the IEA and BloombergNEF (BNEF) suggest this would still take another 20 to 30 years, roughly between 2040 and 2055.

The transition from ICE vehicles to new energy vehicles is a long-term migration measured in decades, far from a stage where ICE vehicles will “suddenly disappear.”

For the Auto Parts Industry, What Truly Matters Is Vehicle Age

The older a vehicle becomes, the more naturally parts deteriorate and failure rates rise, making maintenance and replacement demand more rigid and frequent.

Generally speaking:

0–3 years: primarily routine maintenance, with minimal parts demand;

3–6 years: increasing demand for wear-and-tear parts, with faster replacement cycles;

Over 6 years: significantly higher repair and replacement demand, forming the core of the aftermarket.

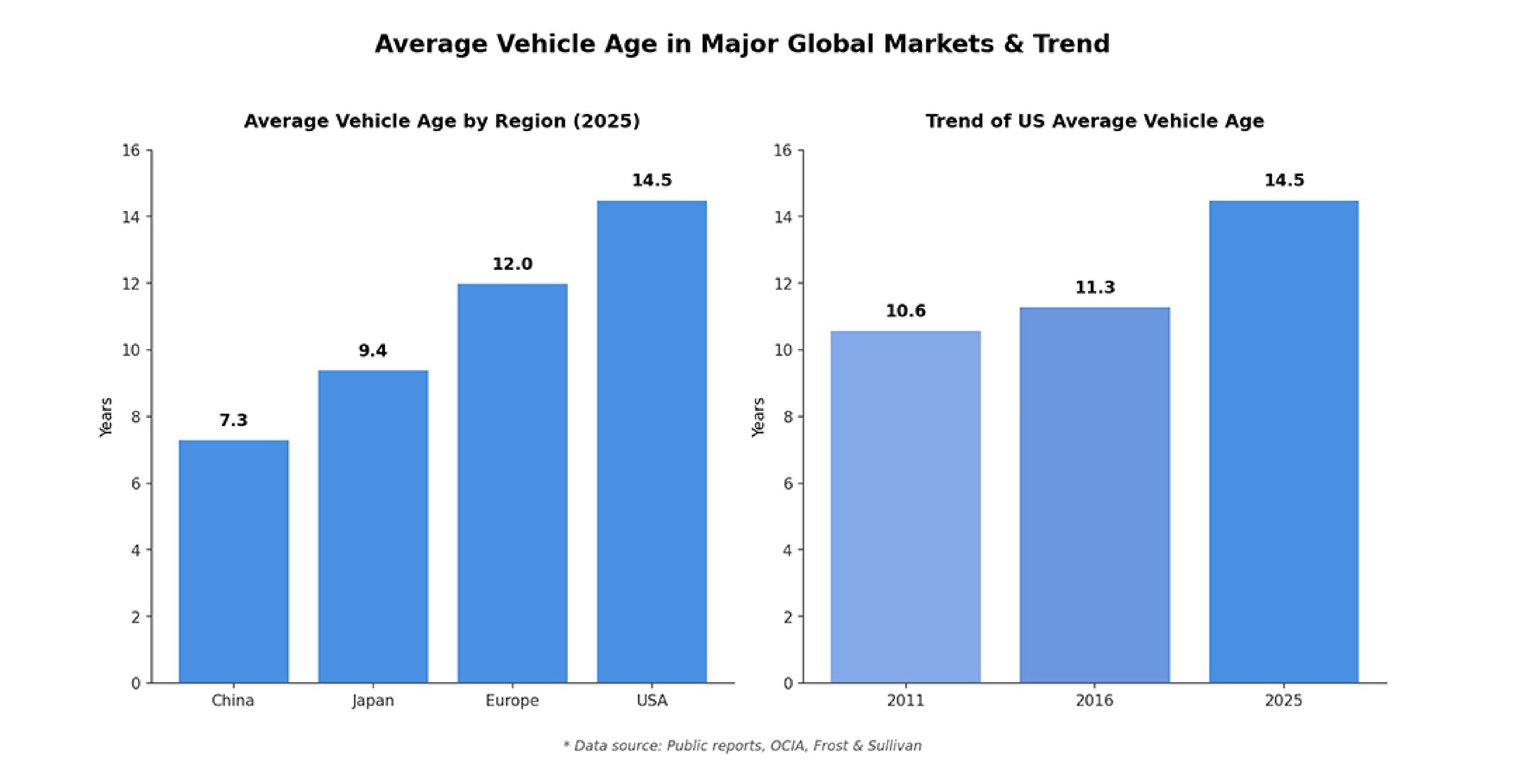

Looking at average vehicle age across major global markets, developed countries have seen a gradual increase over recent decades. In the United States, the average vehicle age has reached approximately 14.5 years; in Japan, it is around 12 years, placing both markets in a highly stable stage for maintenance and replacement demand.

By contrast, markets such as China and Singapore, where vehicle ownership became widespread relatively later, have average vehicle ages of roughly 5–8 years, just entering the threshold of the “deep replacement cycle.”

Mature markets rely on older vehicles to support stable repair demand, while emerging markets are gradually releasing new aftermarket opportunities as vehicle age increases. Against the backdrop of a massive global ICE vehicle parc and steadily rising average vehicle age worldwide, the ICE aftermarket is far from reaching its end, and demand for repair and replacement parts continues to have strong long-term support.

A “Dual-Track” Future

Over the next ten to twenty years, the auto parts market will not follow a path of one-way substitution but rather a dual-track model. On one side lies the vast existing ICE vehicle market; on the other, a gradually expanding new energy ecosystem.

Within the ICE sector, professional suppliers still maintain clear competitive advantages:

stable supply chain resources, SKU management capabilities, brand and channel accumulation, vehicle model and technical expertise, long-term customer relationships, and service capabilities.

These strengths do not suddenly become obsolete simply because propulsion technologies evolve.

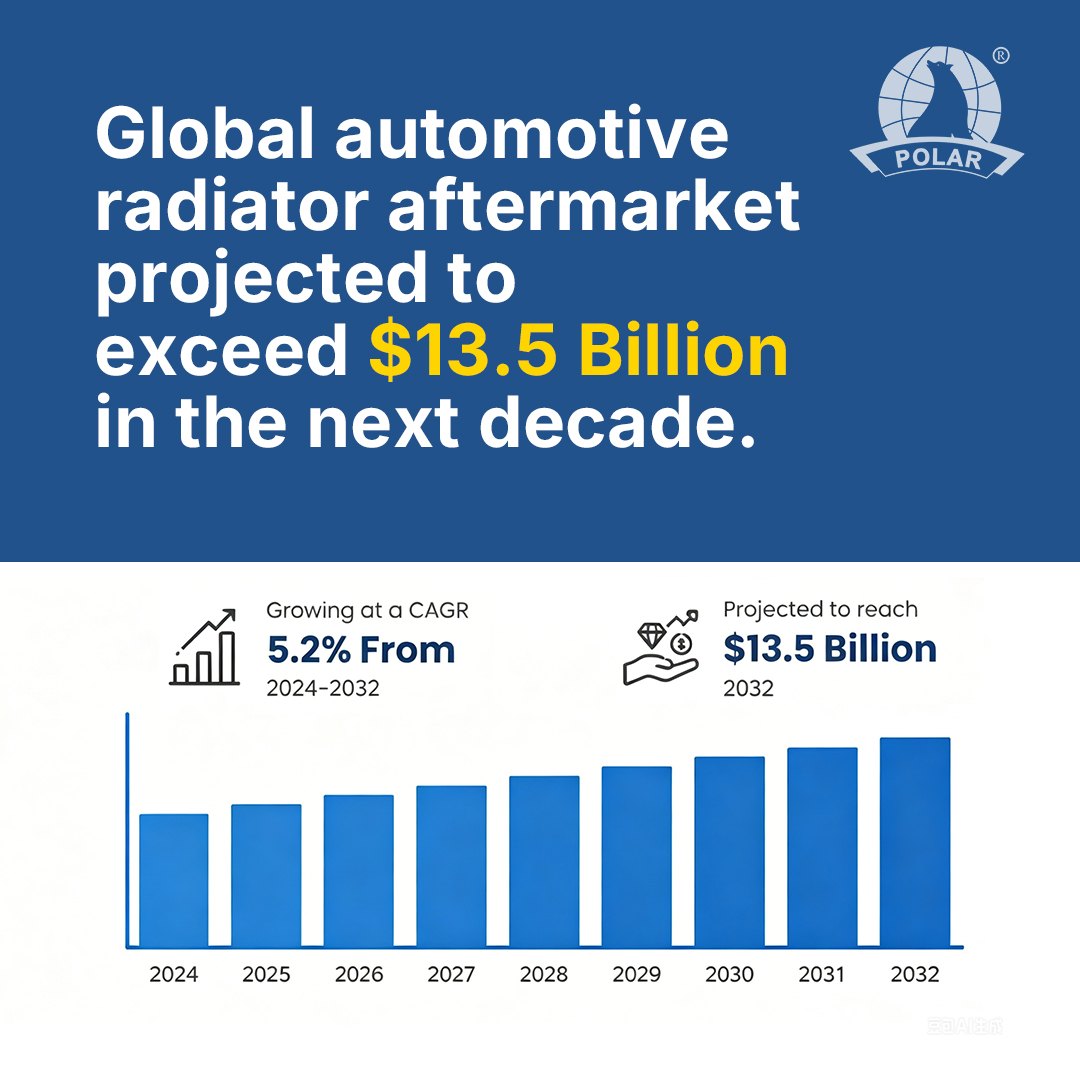

Take the radiator industry as an example.

This is a typical mature component sector, with growth driven by global vehicle ownership and replacement demand, maintaining an overall stable annual growth rate of around 4%–5%. Compared with high-risk, high-volatility sectors such as rapidly expanding NEV markets, foundational components like radiators place greater emphasis on scale, supply chain efficiency, and SKU management—representing a truly long-term business.

The new energy era has undoubtedly arrived, but ICE vehicles will not suddenly exit the stage of history, nor has the ICE aftermarket reached its endpoint.

For professionals in the auto parts industry, the more important question is how to transform existing strengths into the next phase of competitive advantage amid industry change.

Follow FARET POLLAR as we jointly explore global automotive aftermarket trends, seize new opportunities arising from industry transformation, and continue growing and progressing together.

Some of the industry data and trend analysis in this article are based on publicly available research materials and surveys conducted by automotive industry associations. As the chair unit of CAAM, FARET POLAR will continue to monitor global automotive industry developments and aftermarket trends, providing industry partners with deeper market insights and business references.